Do bad index funds exist?

Posted by Mike Limbacher, AIF®, Product Manager on February 21, 2018

Over the past several months, I’ve spoken to several advisors interested in using the new Fiduciary Focus Toolkit™ in their practice. During my conversations, index fund due diligence and monitoring comes up frequently. Several advisors I have spoken to erroneously believe that by simply investing in index funds they can forgo any ongoing monitoring of client investments. This approach is faulty for several reasons, but let’s first examine a more basic question: Do bad index funds exist? Without question the answer is, yes.

Data as of 12.31.17

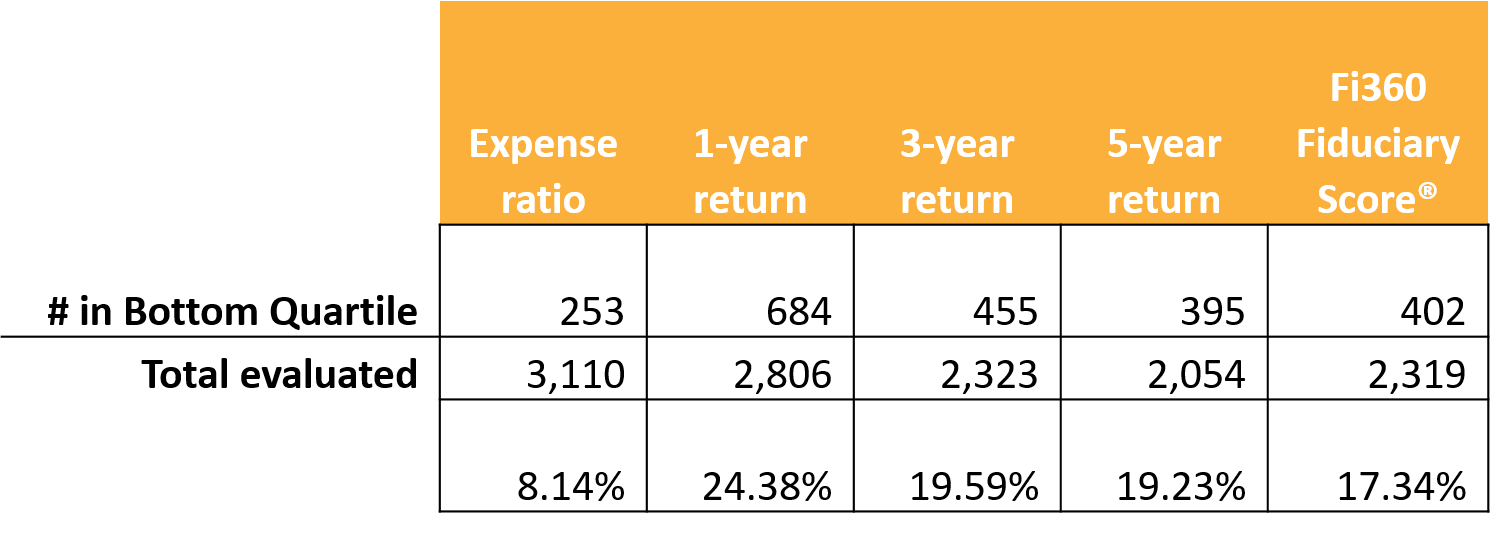

For the period ending Dec. 31, 2017, Morningstar identified 3,110 open-ended mutual funds and ETFs as index funds. Of that group 2,319 received an Fi360 Fiduciary Score®, an evaluation that includes both indexed and not-indexed funds. Of that group, 402 funds, or 17.3 percent, were in the bottom quartile of their peer group. From a fiduciary perspective, we would classify those index funds as poor choices for an investment account and suggest that better options in those funds’ respective peer groups are available.

Let’s look at some performance numbers for the 1-, 3- and 5-year returns of index funds that received an Fi360 Fiduciary Score. 24.4 percent, 19.6 percent and 19.2 percent of all index funds scored fell into the bottom quartile of their overall peer group respectively. Now, a fiduciary evaluation does not demand the best overall performance in a fund’s peer group, however you had better be prepared to explain to a client why a fund remains in their investment mix when it ranks in the bottom quartile.

Finally, let’s examine the expense ratio, a metric where the index fund should have an advantage. Amazingly there are laggards, just over 8.1 percent of index funds were in the bottom quartile. Again, the lowest expense ratio isn’t required, but when the prospect of a low expense ratio is almost expected by index fund investments, a thorough evaluation and documentation process must be conducted if the index fund has an expense ratio in the bottom quartile of its respective peer group.

Regardless of performance, the investments in a fiduciary account must receive a consistent and repeatable evaluation. A cornerstone of a prudent fiduciary process is ensuring that the investment performance of a client account is compared against appropriate index, peer group and investment policy statement objectives.1 Choosing a sort of “set it and forget it” approach by investing in index funds simply does not guarantee prudence.

1Practice 4.1 of the Prudent Practices for Investment Advisors