Anatomy of a Fiduciary Vote

Posted by Duane Thompson on November 06, 2013

Editor's Note: We typically publish on the second and fourth Wednesdays of each month. Due to the upcoming holiday season, we will instead be publishing on the first and third Wednesdays of November and December.

* * * * *

Something unusual happened along the way to a House vote on the ERISA fiduciary standard.

The “Retail Investor Protection Act,” a bill strongly supported by House Republicans to delay the Labor Department’s pending fiduciary rule, was sailing toward passage on the House floor with bipartisan support. Although never expected to pass the Democratic-controlled Senate, the bill was intended to send another "slow down" message to DOL.

H.R. 2374, if enacted into law, would delay or permanently end the DOL’s efforts to expand the toughest fiduciary standard in the financial services industry to securities brokers and ESOP appraisers by permitting the agency to act only after the SEC adopted its own fiduciary rule for brokers.

Earlier in the fall, after several letters from Democrats urged the DOL to go slow on a new rulemaking, half of the party’s members on the House Financial Services committee, or 14 of 28 Democrats, backed up these concerns by voting to pass H.R. 2374 to the House floor.

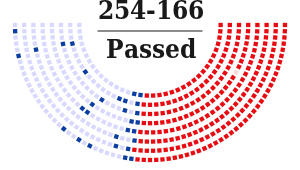

The final floor vote in the House on October 29 was 254-166, passing the bill. It was largely a symbolic vote, but still important for what it said about the state of the politics over a fiduciary standard for pension advice. Republicans voted overwhelmingly in favor, with only a single dissent, and 30 Democrats, or 15 percent of the caucus, joined in support. One independent assessment gives H.R. 2374 a 20 percent chance of becoming law.

Dissecting the anatomy of a fiduciary vote in Congress is a rare occurrence because Congress rarely votes directly on the fiduciary standard. By that measure alone, the vote was significant because Congress, rather than the courts, is increasingly shaping the fiduciary standard for investment advice.

In order to better understand the potential impact of the House vote on future lawmaking, it’s helpful to look briefly at the political jockeying over the previous two years. In November 2011, shortly after DOL withdrew its first rule proposal, 32 Democratic House members pointedly thanked the Labor Secretary for withdrawing the agency’s controversial fiduciary rule. They also urged the Department to “meaningfully and effectively” coordinate its rulemaking effort with the SEC. In effect, industry lobbyists hoped these delaying tactics could actually kill it, knowing the 2012 election could replace the Obama Administration and the rule’s supporters at DOL.

At the time, the Democratic letter created a stir in the trade press. Previously, some House Republicans had sent a similar letter to DOL, but it was quickly forgotten in the wake of the new bombshell from Democratic House members. Shortly after the 2012 elections, though, with the Obama Administration returning for another four years, DOL resumed its work on the fiduciary rule. Assistant Secretary Phyllis Borzi, who had been leading the charge on the new rule, predicted the new version would be released for comment as early as the spring of this year. In June, however, another letter crossed the transom at the DOL. This one was also signed by Democrats – 34 in all, including half of the Congressional Black Caucus. They, too, echoed the industry complaint that the expanded fiduciary standard would drive up costs for investment advice, particularly in light of racial and gender disparities in the savings rate. DOL was again urged to work closely with the SEC on its own fiduciary rulemaking for stockbrokers. Borzi promised to listen to industry complaints but did not back down. In fact, there was increased discussion about expanding the DOL’s fiduciary standard to IRA rollover advice.

About this same time, Rep. Ann Wagner (R-Mo.) introduced H.R. 2374. In September, the House Committee on Financial Services passed the bill, with half of the committee’s 28 Democrats voting for it as previously noted.

Fast forward to the vote on the House floor: the stage seemed set for a fairly strong bipartisan vote. If all the Democrats who signed the letters and the ones who voted for it in committee joined the Republicans, a resounding bipartisan message would be sent to the Senate and give DoL further pause.

Fortunately for opponents of the bill, this is where the rubber met the Beltway and Washington politics. Many of the Democrats who signed the letters or voted in committee suddenly flipped their votes. Washington’s byzantine style of voting on issues may seem odd, but in this instance, not a single member of the Black Caucus who signed the DoL letter voted in favor of the bill. Two other Democratic members who voted for H.R. 2374 in committee voted against the virtually identical bill on the House floor. Two-thirds of the Democrats who signed the November 2011 “go slow” letter also voted against H.R. 2374.

Source: GovTrack.us. Role Call Votes for H.R. 2374. Available here.

So, what happened?

On paper, at least, it might seem that the more liberal the Member’s outlook, the less likely he or she was to actually vote to restrict the fiduciary standard. It’s one thing to sign a letter urging an agency to slow down on a rulemaking; it’s another to put it into statute. The diagram above shows an automated analysis of the vote using a seating chart of the House. Blue represents Democrats and red, Republicans, with the darker shades representing those who voted in favor of H.R. 2374. Placement in the seating arrangement is based on political ideology, using a methodology involving underlying behavioral patterns of each House member. The behavioral patterns are based not on actual floor votes, but on who co-sponsored bills, providing a significantly larger dataset. GovTrack, which developed the methodology, says its results are similar to other tracking methods of actual voting patterns.

In the seating chart, the most liberal Democrats are positioned on the far left, with centrist Democrats represented by those seats bordering the Republican side of the aisle. Thus when you look at the Democratic vote, it’s easy to see that the strongest opposition was from the liberal wing, and the clustering of dark blue votes in the middle indicating scattered support from moderates.

The methodology is buttressed by comparing the same 30 Democratic ‘yes’ votes to Congressional Quarterly’s 2012 ratings based on who voted with the majority of their party on the floor. A significant number of these same Democrats had a weaker correlation to their party’s positions (although CQ does not track voting records of first and second term House members). Based on CQ ratings, the Democrats who voted for H.R. 2374 generally voted with the majority of their party only 76 percent of the time, compared to an average 93 percent of the time for Democratic House members overall. Republicans had a nearly identical voting rate. The single Republican who voted no, Rep. Walter Jones, R-N.C., had a very low 65 percent rating.

This suggests that the floor vote on a fiduciary standard was ideological, in that the more centrist and conservative House members supported status quo regulation.

Strengthening Democratic resolve to oppose the bill was the Obama Administration’s veto threat that was issued the day before the House vote. The Administration’s message was also significant because it is one of the few public statements made since Dodd-Frank reform reaffirming its support for a fiduciary standard for brokers and because it indirectly encouraged the DOL to continue its work on a new rule.

One could also look at the money flowing into the campaigns of House members over the last several election cycles and find a rough correlation as well. However, as tempting as it is to blame money as a corrupting influence in Congress, any analysis connecting a single House vote to PAC contributions would be on shaky ground.

For one thing, nearly all of the opponents of H.R. 2374 have small PACs and are unable to cover the waterfront in the same way as the broader pension industry. The Investment Adviser Association and Financial Planning Association, for example, were opposed and contributed only a tiny percentage of the overall contributions made by the financial services industry to House members and a handful of those members to whom FPA and IAA made contributions voted against their position on H.R. 2374. Ditto for industry supporters of H.R. 2374; many of their contributions went to Democrats who opposed the bill.

Perhaps another factor implicating the voting pattern of the 30 Democrats supporting the bill is that most of them are newcomers to Capitol Hill. Ten of those supporting H.R. 2374 were freshman legislators and 20 of the 30 had served three terms or less. Consistent with the centrist theory, it would suggest that the newer members have far less loyalty to party positions than more senior members. The fact that seven of the 30 Democrats won their seats in the last election by 51 percent or less of the popular vote indicates they come from swing districts and need to demonstrate a more independent voting record.

This brings us to another interesting point, which is the split within the industry itself over the fiduciary standard. I am not aware of any industry surveys based on party affiliation, but anecdotally, the views of the investment advisors I know seem to be shaped more by business model than anything else. In other words, whether you are a registered Democrat or Republican or are independent, common sense suggests that you are four-square behind the traditional fiduciary standard if your firm embraces a fiduciary culture.

This leads to the conclusion that the rationale of an individual Democratic member voting on H.R. 2374, like almost any complex issue, was varied and, like almost any other vote on Capitol Hill, was tied to politics as well as substance. For some, political ideology seems to have played an important role. For others, party loyalty trumped their previous position in letters or committee votes supporting a go-slow approach on the rulemaking.

If there is a silver lining in all this craziness, it’s that the House was exposed to a rudimentary education on the fiduciary standard in the hour-long debate before the vote. The debate itself may have been disappointing to industry insiders, but the pros and cons did cover the waterfront, including costs of suitability versus fiduciary advice. (The debate begins at the bottom of page H6855 in the Congressional Record and is a must-read for anyone interested in this issue.) Even if one is reluctant to award debating points, the discussion before the whole House on H.R. 2374 was an historic debate nonetheless, and one that we may not see again for a very long time.